UPDATE: So here is the justification for using the entertainment tax;

Statute enabling the City to use the Entertainment Tax for promotion.

10-52A-2.   Additional municipal non-ad valorem tax authorized–Rate–Purpose. Any municipality may impose an additional municipal non-ad valorem tax at the rate of one percent upon the gross receipts of all leases or rentals of hotel, motel, campsites, or other lodging accommodations within the municipality for periods of less than twenty-eight consecutive days, or sales of alcoholic beverages as defined in § 35-1-1, or establishments where the public is invited to eat, dine, or purchase and carry out prepared food for immediate consumption, or ticket sales or admissions to places of amusement, athletic, and cultural events, or any combination thereof. The tax shall be levied for the purpose of land acquisition, architectural fees, construction costs, payments for civic center, auditorium, or athletic facility buildings, including the maintenance, staffing, and operations of such facilities and the promotion and advertising of the city, its facilities, attractions, and activities.

Source: SL 2002, ch 68, § 2.

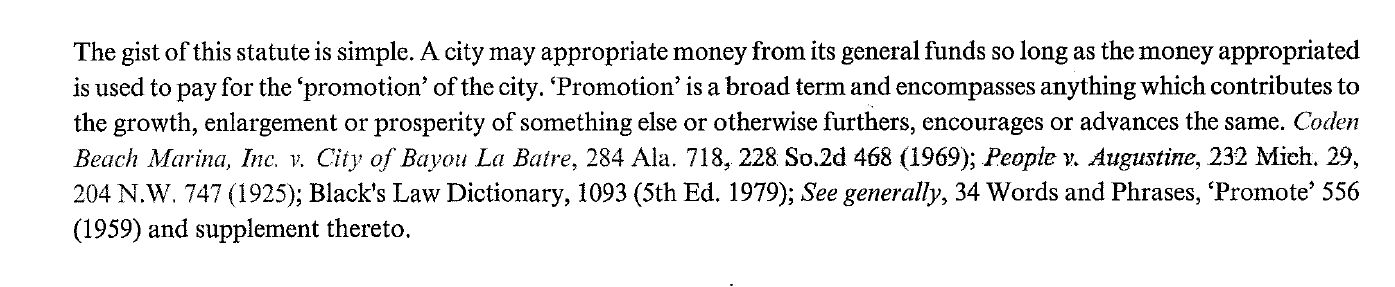

Opinion from Attorney General defining promotion.

From Opinion of Attorney General Mark V Meierhenry  (235) 1984.

$1.5 million is quite a bit to drop for promotion of a non-profit.

According to the press release about the state theatre, this was stated;

The Mayor has pledged $1.5 million to the Sioux Falls State Theatre Company to finance the exterior and structure of the building, life-safety measures, and accessibility. Paired with the gift from Mr. Sanford for the interior completion of the facility, the State Theatre is expected to reopen in 2020.

Using dollars from the City’s Entertainment Tax Fund, the City’s investment in the State Theatre comes from a pool of dollars restricted for culture and entertainment such as the Washington Pavilion and Denny Sanford PREMIER Center Complex.

But according to the ordinance on the entertainment tax, that can ONLY be used for city owned facilities;

SPECIAL TAX RATES.

Notwithstanding the rate of tax established in §§ 37.001 and 37.002, from and after March 1, 1992, the rate of tax upon sales of leases or rentals of hotel, motel, campsites or other lodging accommodations within the city for periods of less than 28 consecutive days; sales of alcoholic beverages as defined in SDCL 35-1-1; sales of establishments where the public is invited to eat, dine or purchase and carry out prepared food for immediate consumption; ticket sales or admissions to places of amusement, athletic or cultural events is 3%. Any revenues received from the tax imposed in this section in excess of 2%, but not more than 3%, shall be used only for the purpose of land acquisition, architectural fees, construction costs, zoo maintenance and operational expenses, and payment for an entertainment center and a convention center, including maintenance, staffing and operations of these facilities and the promotion and advertising of the city, its facilities, attractions and activities.